4 May 2023

Dr. David Allen

Plato is well known for our 100+ Red Flags which are integral to our investment process. These Red Flags have been built up over many years to help identify potential landmines on the long side and also short opportunities.

A question that clients ask time and again is which red flag is the most worrisome? While all of Plato’s Red Flags are linked with poor future stock price performance, one of the most potent is also one of the simplest – negative operating cashflow.

This is the amount of cash a company generates in the course of everyday activities.

A company can have negative underlying earnings, but this can be easily manipulated to give a positive result. Unfortunately, this practice is rife, particularly in Australia.

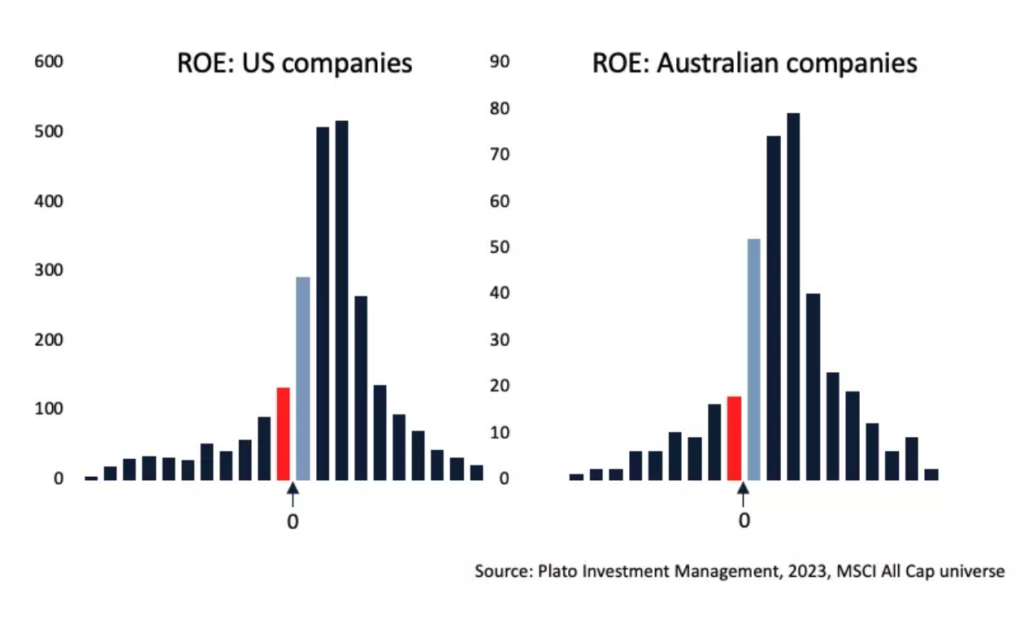

The two charts below show the distribution of ROE (net income divided by shareholder equity) for all US and Australian companies in the MSCI All Cap index.

If companies are distorting the accounts to present a positive net income number to the market, for example by prematurely recognising revenue, then there will be a kink in the distribution at zero.

This is exactly what we see below. There are less red bars (net income just negative) than expected, and more light blue bars (net income just positive) than expected. The kink is much more pronounced in Australia than in the US, which the skeptic would suggest indicates more earnings manipulation.

Because net income is so easy to manipulate, Plato focusses more on operating cashflow. As they say, earnings is an opinion, cashflow is a fact.

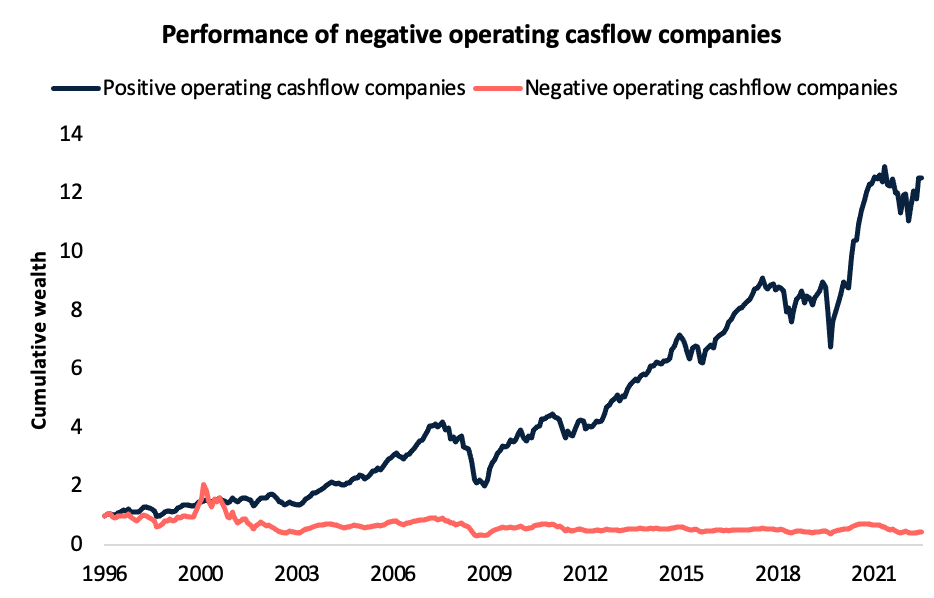

How do companies with negative operating cashflow perform on average? Very poorly.

Below we show the cumulative wealth from investing one dollar in companies with negative operating cashflow (over the prior three years) versus companies that do not for the period 1997-2023. The hypothetical portfolios are rebalanced monthly.

One dollar invested in companies with positive operating cashflow at the start of each month would have grown to $12.37. One dollar invested in companies with negative operating cashflow would have shrunk to a paltry $0.41 with far more volatility along the way. The phrase “return-free risk” comes to mind.

Source: Plato Investment Management, 2023, MSCI All Cap universe

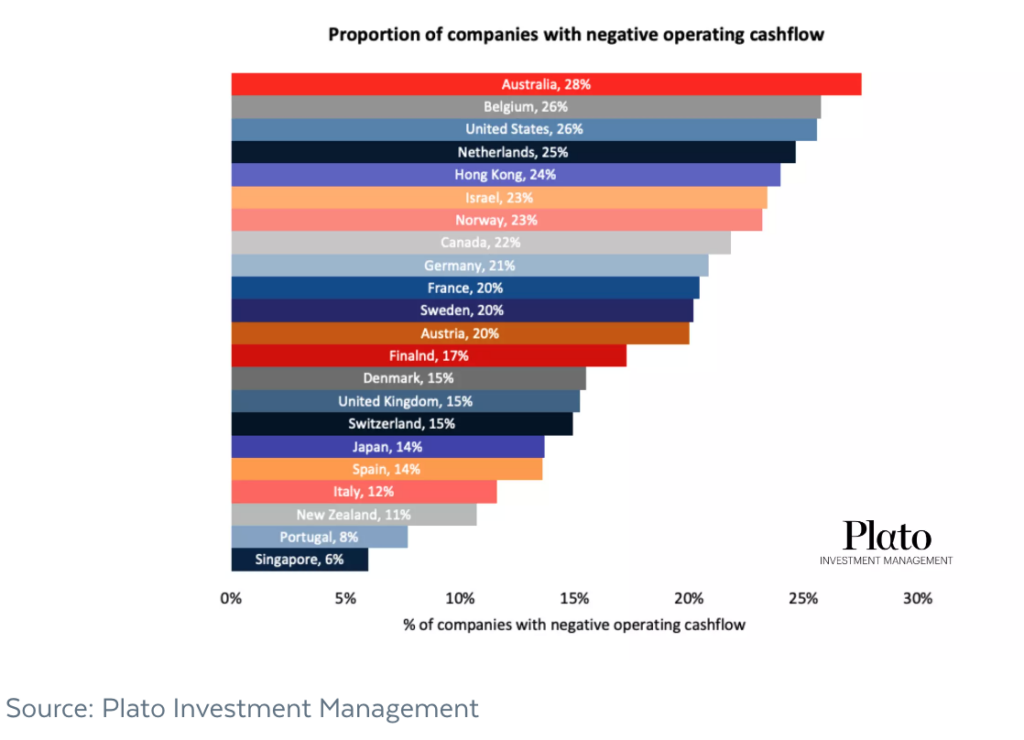

Of particular concern is that Australia has a higher proportion of companies with negative operating cashflow than any other country in the MSCI World index. A whopping 28% of companies have negative operating cashflow over the preceding 12 months.

This of course does not mean Australia is not a good place to invest, simply that is important to be discerning.

The good news is active managers who can sidestep these landmines are well poised. And what this also highlights is why fund investors should consider managers who can short. While a decade-long bull market saw many investors overlook the benefits of a shorting capability, times have certainly changed recently.

About the Author

Dr David Allen is head of Long/Short Strategies at Plato. He holds a PhD from Cambridge and Bachelor of Business with First Class Honours.

DISCLAIMER:

This communication is prepared by Plato Investment Management Limited (‘Plato’) (ABN 77 120 730 136, AFSL 504616) as the investment manager of the Plato Global Net Zero Hedge Fund (ARSN 654 914 048) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement

Link to the Target Market Determination

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Plato, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Plato, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Plato and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future.

Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Plato. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

“A good decision is based on knowledge and not on numbers.”

Plato (427-347 BC)