This Interview with Don Hamson and Peter Gardner Was Published In Livewire.

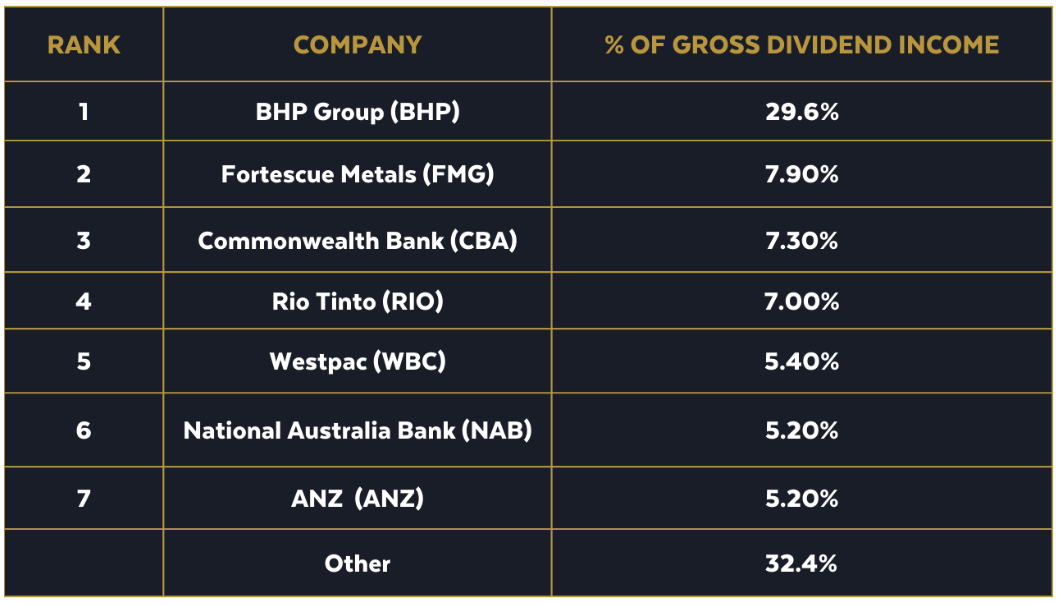

More than 66% of dividends in 2022 expected to come from just 7 stocks

While the 2021 dividend story was all about recovery for Australia’s income-conscious investors, the 2022 outlook is one of stability. That’s the reassuring message from Dr Don Hamson and Dr Peter Gardner from Plato Investment Management, a funds management firm focused on delivering above-market income for their investors.

Hamson says the rebound in dividends that played out in 2021 is largely complete. He expects the market to deliver fully-franked income in the 5.5% to 6% range in 2022, which is in line with long-run averages.

“We’ll do better than that. We expect to get about 9% from our underlying strategies.” Dr Don Hamson, Plato Investment Management

With the ASX200 just sitting in the red for the calendar year, the stable dividend outlook looks likely to play an important role in investor portfolios.

A more challenging environment for total returns

Despite the upbeat picture for income, Hamson and Gardner acknowledge that the total return picture becomes more difficult in a rising interest rate environment:

“Rising interest rates are tough for valuations for all asset classes whether it be houses, infrastructure, shares or even bonds,” Hamson said.

The silver lining for income investors is that strong dividend-paying stocks also tend to be those that have proven most resilient in the recent market sell-off. Commodities producers, energy stocks, and banks have been some of the few bright spots in the local market.

To this point, the ASX200 Resources Index (XJR) is up about 9% and the ASX200 Banks Index (XBK) is up about 5% for the calendar year to date.

Hamson also expects that about two-thirds of all dividends paid from the ASX200 will come from just seven stocks.

The big seven dividend payers in 2022

I recently sat down with Hamson and Gardner to discuss their dividend outlook in more detail. You can watch the discussion by clicking on the player below or read an edited transcript below.

This transcript has been edited for clarity and length

James Marlay: Hi there, folks. We’re here to talk about dividends, one of Australian investors’ favourite topics. And it’s going to be an important part of your returns in 2022, with a growth outlook looking a little bit shaky.

I’m joined today by two people who know dividends inside out, Dr. Don Hamson and Dr. Peter Gardner from Plato Investment Management. Don, 2021, in your own words was the year of the recovery for dividends. What’s 2022 for dividends?

Dr. Don Hamson: The vast bulk of the recovery has happened. I know that there are tourism sectors and others that still have to come back but to be honest, I think they’re going to take a number of years to pay dividends.

Qantas took about seven or eight years after the GFC to pay a dividend. I think it’ll be probably something similar this time around as well.

So, most of the recovery has happened. In the resources sector, I think it’s very much dependent on commodity prices, but we’re still seeing some great dividends there. The rest of the market has largely come back.

We’re still fairly bullish on the banks, and with a rising interest rate environment that actually probably beneficial for banks.

JM: The market at the moment, is really feeling the wobbles with the prospect of higher interest rates, particularly offshore.

But the RBA’s talking about it here as well. What are the flow-on effects for dividend investors or dividend conscious investors like yourselves around higher rates? And that can be a positive or a negative flow-on effect.

Dr. Peter Gardner: In general, obviously, higher rates are going to be negative for market valuations because the discount rates increasing.

But in a relative sense, it’s actually probably positive for high-income stocks, in that if you look at the banks, as Don mentioned, they generally are positively exposed to a higher interest rate environment, and also, the resource companies in that higher inflation, higher interest rate that benefits them as well. And so, in a relative sense, it’s actually a positive for income investors.

JM: And what are some of the specific opportunities? Is it the banks, or are there other sectors that benefit from that rising interest rate environment?

PG: Well, in terms of rising interest rates, there are individual stocks that benefit from it. But generally, when you look at a higher interest rate environment, you’re looking at higher inflation as well. And so, higher inflation generally benefits the commodity players. So energy mining, those stocks, some of the materials as well.

DH: And it’s interesting, I think, on the flip side though, if you actually look at the volatility and where the real impact of higher interest rates is, it’s generally speaking in the growth stocks, and crypto and areas like that, which are speculative because investors, when interest rates start rising, they want real money.

They can get higher interest in the bank, but they can also get good dividends out of the traditional income payers, but they’re not as focused on growth. So you’ve seen most of the volatility actually in those growth stocks, which obviously don’t pay much dividends.

JM: So, if we look at the Australian market, if we’re looking out towards 2022, what are some of the trends that you’re observing, particularly at the management level and particularly for people like yourselves that can take advantage of tax efficiencies from buybacks and the like.

DH: Well, we’ve seen quite a few tax-efficient buybacks on off-market buybacks from CBA, Woolworths, just one recently from JB Hi-Fi.

So there’s been a good return of capital and some very tax-effective payments, particularly for low tax investors and zero tax investors, which is our target market.

Another interesting one is that BHP is looking to spin off its oil and gas assets to Woodside. That’s actually going to be from a tax purpose considered to be a fully franked dividend, and BHP will attach a very large franking credit to that spinoff if you like.

So, particularly for low-tax investors, they’re going to get this huge franking credit bonus if they own BHP. So that’s one to look out for if you’re a BHP investor. So, certainly, some good tax opportunities out there and franking credits are still very valuable.

PG: Yeah. One of the other trends is in the mining space that when we’ve seen previous commodity price booms, you’ve seen a huge amount of reinvestment, and a lot of that money that has come to miners then has been reinvested and hasn’t necessarily been paid back to shareholders.

But in this case, it does look like all the miners are staying very disciplined and not actually building a lot of new mines or purchasing other assets. And so, that’s been a positive in terms of how much income they can return to investors.

JM: The iron ore mine has really led the charge with that discipline. Do you expect other commodity players to take the lead from the likes of BHP, and Rio, and Fortescue that have paved the way on that front?

PG: Definitely, on the oil stocks, that is the case, but it’s a bit more nuanced, and that’s dependent on the tax situation of each company.

In the case of Woodside, they’ve got a huge level of franking credits in terms of their franking credit balance that they’ve got on their balance sheet.

And so, they’ve actually got the ability to do an off-market buyback if they wanted or to pay a lot of special dividends.

But on Santos, on the other hand, doesn’t have a big franking account balance, and so, they’ve just announced it recently that they’re going to up their payout ratio, well, they haven’t said how they’re going to do it, but in this case, they’ve done it in the form of an on-market buyback of 250 million dollars.

They’ll be returning the cash because they don’t have the franking credits in order to do it in a more tax-efficient manner. In terms of other commodities, there are certain lithium miners that are becoming a bigger part of their index. I expect them to be reinvesting most of the money they’re earning at the moment.

And then South32’s probably another one that should be increasing its payout as well as a result.

JM: And what about gold miners?

PG: They generally have a lower payout and yeah, we expect that to continue going forward. It doesn’t seem to be any major change, but we’ll look out for that.

JM: A watching brief with the gold miners. Okay. Now, we touched on the banks a little bit earlier. And Don, you said you were still mildly positive or quite upbeat on the outlook for the banks.

Can you talk me through in a bit more detail how you see the dividend outlook for Australia’s big four, and if there are any standout players that you think have the ability to either increase their dividend, or do specials, or whatever it might be.

DH: Yeah. If you go back over the last three or four years, there’s been a lot of headwinds for banks. You’ve had Royal Commission. You’ve had a lot of remediation. A couple of the banks have had AUSTRAC issues. So, you’ve had a huge number of, I suppose, negatives, which are slowly falling off.

So we’re actually getting rid of the negatives, which means earnings should be stronger.

The other headwind has been lower interest rates because we’re basically a zero interest rate environment, and so, it was very hard for the banks to increase their margins in that situation.

But now that it looks pretty apparent that we’ll see rising interest rates … that is usually a more favourable environment for banks where they can increase their margins.

And you’ve also got fairly positive housing outlook still at the moment, although if interest rates rise too rapidly, that could change. But I don’t think the RBA will be raising rates too fast.

Obviously, inflation’s probably a huge trend at the moment, globally, but if you look at our latest inflation, it’s 3.5%. It’s like six or 7% in Europe and the US. Our level of inflation’s nowhere near, and even in New Zealand, I think it’s about 6%.

So, yes, we have in inflation, but it’s not that far away from the target for the RBA, whereas overseas is clearly extremely high, so that’s why they’re pushing their rates up quite rapidly.

JM: Now, Australian iron ore miners are effectively the new blue-chip dividend stocks in the market. I was blown away to see that they rank in the top 10 dividend payers globally, which is quite staggering: BHP is number one.

Plato was really early on that call. I remember seeing articles come up on the Livewire website, and people say miners don’t pay dividends. Miners aren’t dividend stocks. And that was three odd years ago now. So what does the future hold for the dividend outlook, particularly for Australia’s big three iron ore miners?

DH: I think the outlook is still pretty good. In the short term, you still have low levels of supply of high-quality iron ore, which Australia has been repeatedly underperforming and missing its targets in terms of production.

As China opens up, obviously, they’ve been closed a lot, I think that will spur demand as well. So, we’re still pretty bullish, but clearly, it is a commodity that can go up and down.

But I think one of the reasons why we’re on this early and it’s a positive theme is there’s been incredible good capital management by the banks.

As Peter said before, they’re not racing out and building massive amounts of mines, they’re actually being very disciplined, and they’re returning that money to shareholders.

Now, the one exception is probably Fortescue. I think it’s probably the weaker of the three for two reasons. One, its iron ore is lower quality, but secondly, and it may turn out to be very good but it’s investing a lot of money into its green hydrogen and other things for its future growth.

So, if you are investing, you’re not returning it to shareholders. So, they were probably the weaker of the three in terms of the last reporting season.

JM: Do you think the oil and gas producers can emulate what has been happening in the iron ore space.

DH: Well, I think you’re right there. If you look at it, there’s been a global lack of investment into oil and gas because, clearly, I think people are looking at the transition to renewables and those sorts of things, but as we’ve seen, and it wasn’t just the Ukraine war that caused this, oil and gas prices have been going up for the last 12 months.

The reality is there is a shortage of supply, and renewables are going to take a long time to come on board. So for the next 10, 15 years, I think there’s actually a purple patch, particularly for cleaner energy, such as natural gas to fill that void until the renewables come through.

And because there hasn’t been a huge amount of investment, there is actually a lack of supply, and if you take Russia out of the equation, then it’s very, very good for the likes of Woodside and Santos.

JM: In your analysis do you think about what could be a scenario where the pricing pressure eases? I know you were quite early with the iron miners.

You did think a lot about what could be behind the price, where could it go to, not trying to pinpoint the forecast, but putting some thought into it. Have you done the same on oil?

DH: Well, the reality is, whilst we have a longer-term view and a view about these things, we track commodity prices every day.

So, whilst our preferred view for both iron ore and natural gas is pretty good, oil and gas, things can change on a dime.

I still think there’s going to be this nice little period for the next 10 or so years before renewables come on board. So I think the pricing outlook is pretty good, but we monitor it daily.

PG: The other side is the China lockdowns, There’s talk of Beijing starting to go into lockdown. And so that’s putting some short-term pressure on the oil price as well. As Don says, we’ll monitor how that situation goes because it’s hard to know if the China government suddenly announces they’re moving away from zero COVID then that strategy, then you’ll suddenly see a spike in the oil price again, probably, as their cities open up.

JM: Now, Livewire readers and viewers love a good statistic and a good chart. And I’ve asked Plato to put together a chart or pick a statistic that they think summarises or encapsulates the dividend opportunity for the rest of 2022.

So, what’s the chart that you’ve brought along or the stat that you’ve brought along, and what’s the story that it tells?

DH: We’ve been showing this chart for the last couple of years, and I think it’s told the story of the pandemic and the impact on dividends. It’s a chart of the average probability or the probability of a dividend cut at the market level.

So we basically aggregate up as part of our process. We look at each stock and look at the probability that it might cut its dividend. It’s based on individual stocks, but then we aggregate it up at the market level and it gives us a market picture of the dividend outlook.

DH: And if you look at that chart, the first stage of the pandemic stands out like the proverbials because it went through the roof to the highest likely ever possibility of a dividend cut at the market level, like about 45%, and we saw massive dividend cuts.

But it’s actually tracked back very quickly after that, which was one of our calls last year, while we thought dividends were going to be quite strong because it came back to below normal.

And now, it’s just ticked up to about average at the moment, which means we’re in a pretty good position. A normal position now for dividends, which is not bad. We’ve seen the big recovery last year, and now we’re seeing a pretty stable outlook for dividends.

JM: From the discussion we’ve had today, it sounds like the sources of income are quite broad-based. Banks are okay. Miners, a good spot. Some potential alternative options in the oil and gas sector as well.

DH: Yes, but the banks and the iron ore miners now represent about two-thirds of all dividends paid in the Australian market. The outlook, to us, looks pretty good for those two sectors, which is positive.

But it does still mean though, that Australia is a pretty undiversified place because, really, the resources and the banks are most of our market, but they’re doing pretty well at moment.

PG: It speaks a bit to the Plato process that, I guess as an investor, you could just invest in those individual stocks, but then you don’t get access to some of the other areas of the market as well.

And so part of our process is holding some of the alternative areas of the market too, that aren’t necessarily high yield so that we can get the total return as well as the income and trade that off.

JM: Let’s talk about total returns. I know you do a lot of modelling and a lot of forecasting. What sort of returns are you expecting Plato to be able to deliver over the next 12 months from an income perspective?

DH: I must admit we hedge our bets and turn to total returns because clearly, total returns are going to be very dependent on the market outlook and what the market’s doing and, particularly this year, on what interest rates are doing.

On that front, I would say 2022’s going to be a much more challenging year than 2021 because we now have the spectre of higher interest rates, which we really haven’t seen since around 2009.

So, it’s a long time since we’ve seen a rising interest rate environment, and rising interest rates are tough for valuations for all assets, whether it be houses, whether it be infrastructure, shares, or even bonds. We might actually see negative returns on bonds if interest rates spike up.

So, it’s going to be tough from a total return point of view.

What I can say is that we think the outlook for dividends is pretty strong, and we think the market will probably generate, including franking credits, somewhere between about five and a half to 6% dividend return this year

But the capital could quite conceivably go backwards if we see interest rates rise more than what the market’s currently expecting.

JM: And how does that five to 6% compare to long-term average?

DH: That’s about the long-term average, actually. So we’re about back to where it was pre-COVID.

JM: The full recovery.

DH: Yep. Of course, we’ll do better than that. We probably expect to get around 9% from our underlying strategies this year.

Don’t miss out on a piece of the dividend pie

Plato Investment Management is dedicated to helping retirees get more from their share portfolios. You can learn more about the Plato Australian Shares Income Fund here.

SUBSCRIBE TO OUR NEWSLETTER

Subscribe to keep up to date with the latest fund

information and insights.

“A good decision is based on knowledge and not on numbers.”

Plato (427-347 BC)

Disclaimer

Plato Investment Management Limited AFSL 504616 ABN 77 120 730 136 (‘Plato’).

Whilst Plato believes the information contained in this communication is based on reliable information, no warranty is given as to its accuracy and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Plato disclaim all liability to any person relying on the information contained on this website in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information.

Pinnacle Fund Services Limited ABN 29 082 494 362 AFSL 238371 is the product issuer of funds managed by Plato. Any potential investor should consider the relevant Product Disclosure Statement available at https://plato.com.au/retail-funds/ in deciding whether to acquire, or continue to hold units in a fund. The issuer is not licensed to provide financial product advice. Please consult your financial adviser before making a decision. Past performance is not a reliable indicator of future performance.

Disclosure contained on this website is for general information only. Any opinions or forecasts reflect the judgment and assumptions of Plato on the basis of information at the date of publication and may later change without notice. Any projections are estimates only and may not be realised in the future. Information on this website is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained on the website is prohibited without obtaining prior written permission from Plato. Past performance is not a reliable indicator of future performance.