On Monday 23rd November, Ampol (formally known as Caltex) announced a $300m off-market buy-back after finalising its property transaction where it raised $635m after tax.

Off-market buy-backs are a tax effective mechanism for returning franking credits to shareholders who most value them. The buy-back will have a $2.01 capital component, with the balance being a fully franked dividend. The buy-back will be based on a tender, with investors tendering to sell shares at a discount of between 10% to 14% below market price. Shareholders who don’t participate will still benefit from the buy-back, to the extent that shares are effectively bought back at a cash discount to market price. This compares with on-market buybacks, where companies buy-back stock at market price.

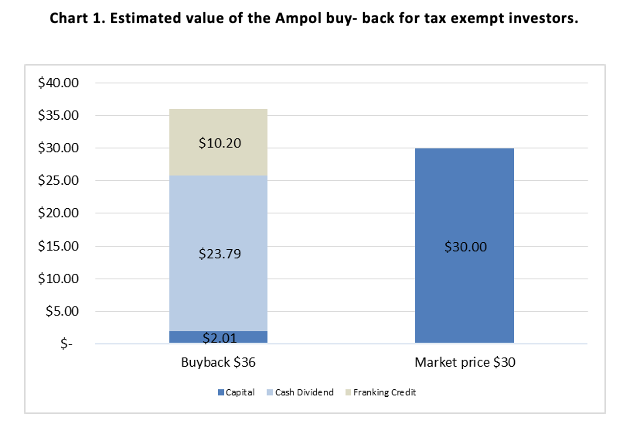

We have analysed the value of the buy-back for tax-exempt investors such as charities, foundations, pension phase superannuation and individuals below the income tax threshold using the market price of Ampol at the time of writing on November 24 of $30.00 – see Chart 1 below. Using $30.00 as a guide (the actual price used for the buy-back will be the volume weighted average price of Ampol shares in the five trading days up to and including January 22, 2021) the maximum 14% discount would equate to a $25.80 buy-back price. With the capital component being $2.01, the other $23.79 would represent a fully franked dividend, which would have a $10.20 franking credit attached. For a tax-exempt Australian investor, we estimate the buy-back at a 14% discount would be worth approximately $36.00 (disregarding the time value of money), representing about $6.00 or 20% more than the market price of Ampol today, but please note that the buy-back is expected to be completed on January 25, 2021, based on volume weighted prices from the previous week.

The value of the buy-back for other investors will depend on the tax situation of each investor. We would expect the buy-back to be of some value for 15% tax rate Australian investors, but significantly less that the 20% number for tax-exempt investors. The precise value will be determined by investor circumstances, the deemed capital value that the ATO will issue after the close of the buyback and the final buy-back price relative to the closing market price.

Given that we estimate the buy-back is valuable for both tax-exempt and 15% tax rate Australian investors at the maximum discount rate, and given the moderate size of the buy-back relative to Ampol’s current market capitalisation (approximately 4%), we would expect the final buy-back price to be set at the maximum 14% discount to market price. We would also expect, based on similar buy-backs, that the buy-back will be oversubscribed and thus investors would be likely subject to potentially large scale-back (other than small investors who would be left with less than 75 shares as a result of the scale-back) – that is only a small portion of shares tendered would be successfully bought back in the buy-back. So whilst we expect the buy-back to be quite valuable for tax-exempt Australian investors for every share successfully tendered, any scale-back will reduce the overall value of the buy-back at the portfolio level.

Plato expects to tender all Ampol shares owned by the Plato Australian Shares Income Fund into the buy-back as this fund is managed from the perspective of tax-exempt Australian investors. This means that investors in both the Plato Australian Shares Income Fund and Plato Income Maximiser Limited (PL8.AX) should benefit from the Ampol buy-back. We believe opportunities such as this Ampol buy-back highlight the importance of tax-exempt investors like pension phase superannuants having their investments managed from their tax perspective.

Please note that this analysis depends very much on the particular tax status of the investor. We would suggest individual investors should seek professional tax advice based on their individual tax circumstances.

SUBSCRIBE TO OUR NEWSLETTER FOR MORE INCOME INVESTING INSIGHTS

SUBSCRIBEDISCLAIMER:

This document is prepared by Plato Investment Management Limited ABN 77 120 730 136, AFSL 504616 (‘Plato’). Pinnacle Funds Services Limited ABN 29 082 494 362, AFSL 238371 (‘PFSL’) is the product issuer of the Plato Australian Shares Income Fund (‘the Fund’). The Product Disclosure Statement (‘PDS’) of the Fund is available at https://plato.com.au/. Any potential investor should consider the relevant PDS before deciding whether to acquire, or continue to hold units in, a fund.

Plato Investment Management Limited (ABN 77 120 730 136, AFSL 504616) (‘Plato’) is the investment manager of Plato Income Maximiser Limited ACN 616 746 215 (‘PL8’ or the ‘Company’). PL8 is the issuer of the shares in the Company under the Offer Document. Any offer or sale of securities are made pursuant to definitive documentation, which describes the terms of the offer (‘Offer Document’) available at https://plato.com.au/lic-overview/ This communication is not, and does not constitute, an offer to sell or the solicitation, invitation or recommendation to purchase any securities and neither this communication nor anything contained in it forms the basis of any contract or commitment. Prospective investors should consider the Offer Document in deciding whether to acquire securities under the offer. Prospective investors who want to acquire under the offer will need to complete an application form that is in or accompanies the Offer Document. The Offer Document is an important document that should be read in its entirety before deciding whether to participate in the offer. Prospective investors should rely only on information in the Offer Document and any supplementary or replacement document. Prospective investors should contact their professional advisers with any queries after reading the Offer Document.

Plato and PFSL believe the information contained in this document is reliable, however no warranty is given as to its accuracy and persons relying on this information do so at their own risk. This communication is for general information only and was prepared for multiple distribution and does not take account of the specific investment objectives of individual recipients and it may not be appropriate in all circumstances. Persons relying on this information should do so in light of their specific investment objectives and financial situations. Any person considering action on the basis of this communication must seek individual advice relevant to their particular circumstances and investment objectives. Subject to any liability which cannot be excluded under the relevant laws, Plato and PFSL disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information.

Any opinions or forecasts reflect the judgment and assumptions of Plato and its representatives on the basis of information at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. The information is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. Past performance is not a reliable indicator of future performance.

Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this document is prohibited without obtaining prior written permission from Plato. Plato and their associates may have interests in financial products mentioned in the presentation.